Estimating Lending Club's ROI (a survival food interlude)

Aug 11, 2010, 11:56p - Investing

Some of you may be surprised that my mind is working at all given my limited diet. Since so few have actually undertaken my survival food experiment, I think expecting your mind to give way may be an unrealistic expectation. I believe that most people would recover to some decent level of performance even though they'd only be eating ~1500 calories per day, like I have. That may not be true, but we'll never know if no one else tries it. I think my survival school buddies did just fine, though they didn't have much mental work in front of them in the wilderness. Also, I'm reading a book on the Minnesota Starvation Experiment (done in the '40s), and my sense is they were just fine (mentally-speaking) after 4 weeks of ~1500 calories per day.

Anyhow, back to the issue at hand. Yesterday, instead of devoting my attention to a new C. elegans-related program I've been working on, I took a break and did some more analysis of Lending Club investments. You may remember my last post about this, where I showed that with some fancy programming (in the form of a support vector machine - read the post if you're curious about what that is) I could significantly improve returns on the peer-to-peer lending site Prosper.com. I also showed that it had a negligible impact on another peer-to-peer lending service called LendingClub.com. Here I will describe an analysis that shows (what I believe to be) the realistic returns that one should expect if investing on Lending Club. This analysis also breaks down the return by credit grade.

Lending Club advertises an annual rate of return of 9.65%. That sounds pretty high, especially in these volatile economic times. As a point of comparison, the stock market has historically appreciated 8-10% annually, and homes tend to appreciate 6-10% annually (depending on location). Lending Club calculates a 9.65% ROI (annual return on investment) by looking at the ROI for all loans made since their site's inception, except those made in the past 4 months. The reason they exclude the last 4 months is that loans rarely default so quickly after being originated, and if they included those loans the ROI (return on investment) would be skewed higher and would be a poor estimate of true return.

The problem with this estimate, though, is that a huge portion of the loans they include in their calculation still haven't had much time to default (as little as 5 months). The loans are for 3 years. So I've been suspicious of Lending Club's advertised ROI for a while, and I didn't believe that it was an accurate estimate of the true rate of return. So I decided to do some math of my own.

The most conservative ROI estimate would only include loans which have completed their 3 year term. The problem with this approach is that Lending Club is such a new company that for a while it didn't have any loans that fit this criteria. This has now changed. Lending Club started issuing loans in June 2007, and since we're now sitting in August 2010, this means that just more than 3 years have passed for these early loans. Of course, it usually takes something like 4 months late for a loan to be categorized as defaulted, but we'll ignore that detail for now.

So using the ROI statistics available on Lending Club's site, I decided to calculate this conservative ROI, which I'll call the "Finished ROI". The Finished ROI only includes the return on loans made in June and July 2007, and nothing more recent than this. The number of loans may be small (e.g. there were only 19 grade A and 2 grade G loans during this time interval), but it's better than 0. The Finished ROIs are broken down by credit grade and shown below in Table 1:

| Grade A | Grade B | Grade C | Grade D |

Grade E | Grade F | Grade G | Average |

| 5.81% | 5.42% | 5.88% | -16.89% | 14.07% |

0.51% | 17.22% | 4.57% |

Table 1: Finished ROI by Credit Grade

Now as I mentioned, the number of samples in each column is pretty small (somewhere between 2 and 20), so I wouldn't extrapolate too much from this data. So for my next ROI estimate I decided to take a weighted average of all the loan ROIs made to date, where each loan ROI's weight is inversely proportional to the age of the loan. So older loans have higher weight than younger ones, in a linear fashion. I'll call this the "Weighted ROI" estimate, and it includes loan data from June 2007 to July 2010. The results are shown in Table 2 below:

| Grade A | Grade B | Grade C | Grade D |

Grade E | Grade F | Grade G | Average |

| 6.27% | 4.38% | 5.04% | 2.97% | 6.34% |

-0.01% | 7.91% | 4.70% |

Table 2: Weighted ROI by Credit Grade

One caveat of both the Weighted ROI and Finished ROI estimates is that they both weight months and credit grades equally, regardless of the number of loans made during that month. This is a detail that requires further investigation, but it's one that I'm not interested in pursuing at the moment.

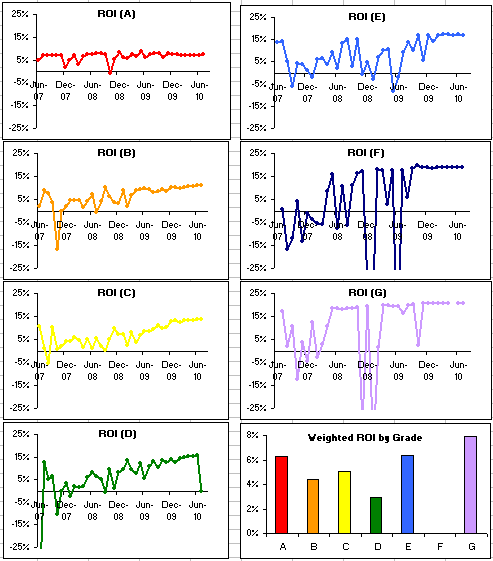

I plotted the ROI by month that loans were issued, as well as a bar chart that shows the Weighted ROI by loan grade. See Figure 1, which is a screenshot taken from my Excel spreadsheet:

Figure 1: ROIs listed for each credit grade as a function of the month the loans originated. The final graph plots the Weighted ROIs from Table 2 as a bar graph.

So what's worth taking away from this analysis?

- The Weighted ROI across all loans is 4.7%, about half of Lending Club's own advertised number of 9.65%, ignoring the inaccurate calculation made by weighting all loan grades equally. Even if the number of loans in each loan grade were taken into account, it's hard to see how one could hit 9.65%, since the highest weighted ROI is 7.91%. Since I believe that the Weighted ROI is a more accurate estimate than Lending Club's own estimate, I think that they're misleading prospective lenders with an inflated and inaccurate estimate.

- Loans with grades of A, E, and G perform the best, with Weighted ROIs of 6.3%, 6.3%, and 7.9% respectively. I'm not sure why grade E and G loans are doing so much better than F loans (which are earning 0% Weighted ROI), so this may be something to investigate further. Maybe Lending Club's grade-setting algorithm is out-of-whack?

- Volatility increases with loan grade, as shown in the graphs of Figure 1. I quantified this by measuring the standard deviation of each grade, which I won't present here (leave a comment if you're interested in these numbers). I'm not quite sure why this is the case.

Overall, I conclude that if you're going to lend on Lending Club, stick to grade A borrowers. If you're adventurous, consider lending to grade E and G borrowers as well. If you follow this policy, you should expect an ROI somewhere between 6 to 8%.

Of course the data above is only valid today, as tomorrow new data will be available that could change these results. If I'm inspired, I may set up a page which always has the most up-to-date analysis.

Finally, Lending Club is still a new service (just over 3 years old), so it's possible for things to change dramataically in the future. What I've presented above is my most reasonable estimate of what the future might hold, but as with all future-predictions, it may very well be wrong.

Leave a comment if you have any questions or comments, or if you think of a better way to estimate Lending Club's ROI.

--

- Data Source - Lending Club's performance page

- How Lending Club calculates ROI for each loan

Read comments (7) - Comment

Sachin

- Aug 12, 2010, 7:29p

You spend a lot of time doing all this analysis. I'd just let a financial advisor take care of it. Or just stick it in a CD and save myself the headaches and stress.

Or if I want to help people who can't get loans, I'd just give money to Kiva (I do).

nikhil

- Aug 14, 2010, 6:58a

I've worked with several financial advisors, and none of the ones I've met do any of this. Maybe I haven't met the right person yet, but I've looked. Most haven't even heard of Lending Club.

CDs don't get anywhere near this level of return (assuming this pans out as hoped) - the highest rate on bankrate.com is 2.4% for a 3-yr CD (compare to 6% I'm hoping on Lending Club). Of course, this makes sense - Lending Club is riskier, takes more work than a 3-yr CD, and doesn't have the FDIC insurance).

Also, I want to help people AND get a good return, so Kiva isn't the right place for me.

Finally, I actually find doing this analysis fun :) I have a question that pops into my mind, and I answer it. Very satisfying (just like engineering can be). And it only took me 1 day, so not much time at all :) The previous SVM post did take me quite a bit longer, though, but I was learning the whole way through.

Connie

- Aug 14, 2010, 4:45p

Good to see you and B last week :) I came to your website to see how you're faring on Day 21, and here you are ranting about Lending Club again, haha. Anyway, the other site I was telling you about is microplace.com. My preference over Kiva. Microplace used to have more investments for 3%+ (and yes, I've been getting my funds back, no defaults yet after 3 years) so take a look and see if it works for you. Um, no insurance there either.

I would guess that financial advisors would prefer that you either invest in stocks or in mutual funds or other financial instruments as they get to make some money off the transaction. And the back analysis is usually done by someone else. Lending Club = no kickback + too small to be worth it for really rich people.

Two more things on the survival diet front. First, women's diets sometimes go all the way down to 1200 calories - just was reading about a few of the popular diets in a women's mag. Liquid diets are the rage. Also, there are lots of people fasting for Ramadan right now, which apparently may or may not work that well as there are giant parties every night where you (can) gorge yourself silly. Ah, the things we do for religion.

Write again and let us know how you're doing.

Barbara

- Aug 23, 2010, 5:04p

Although I am sure that your analysis has merit, it presumes that an investor invests equally in all loans. I believe that my strategy for investing in LC loans serves to increase return and lower risk for me personally, as opposed to all loans overall. There are many factors that I take into consideration when I evaluate which loans to back but I will give you a very easy example - I never invest in small business loans (even at a min. buy-in of $25, who invests in a small business w/o even seeing the business plan?) Also, I rarely invest in anyone who is applying for the max. amount - $25,000 just happens to be the amount that they need? More likely they are the type who are living in a hole and they are likely to dig it even deeper.

nikhil

- Aug 24, 2010, 3:22p

I agree with you Barbara. I also have various criteria that I layer on top of a borrower's credit grade before deciding to lend money. Expected return under those conditions are a bit harder to estimate, but in some cases also feasible.

Colin

- Sep 19, 2010, 11:21a

Hey Nikhil,

Great idea to take a different perspective on the ROI. Aside from getting into the details of whether your figures are right, it is important to let people know the difference between the advertised ROI and what they might find after 3 years.

I myself have spent a lot of time recently studying into the industry and definitely think it deserves the kind of attention you are giving it.

Cheers,

Colin

Mike

- Dec 13, 2010, 3:51p

I've been looking for something EXACTLY like this..

I've been looking to hunker down $50k or so into LC, but have been suspicious of their high rates and held off...

Please keep updating this post and do you have a website that does so??

Favorited..

Thanks Mike

« 28 Days of Survival Food: Day 16

-

28 Days of Survival Food: Day 22 »

|