What the LendingClub IPO reveals about its business

Dec 4, 2014, 3:01p - Investing

LendingClub is planning an IPO soon, probably on or after December 10, 2014. In this post, I will discuss why I think the standard view of LendingClub as a peer-to-peer (P2P) finance service will become outdated. Specifically, I will show that a larger portion of LendingClub's loans are being funded not by other individuals but by institutional investors, such as banks. That fact, combined with a reduction in the growth of loans funded by individuals, suggests that the company might evolve into another sales arm of the traditional banking industry. Rather than remaining a P2P finance company, LendingClub appears poised to become a middleman linking the needs of borrowers with the funds of banks across a larger set of credit categories.

Background: What LendingClub does

LendingClub began as a peer-to-peer (P2P) financial service in 2007. The basic idea is that instead of borrowing from a bank, borrowers borrow money from individual lenders, regular people like you and me. Borrowers win because they get lower interest rates: for example, if you have good credit, you can refinance your credit card balance and effectively lower your interest rate from 30% (what a standard credit card charges) down to as low as 6% (the lowest interest rate available on LendingClub). Lenders win because they get higher interest rates on their cash. For example, the standard term of a LendingClub loan is 3 years. Currently, certificates of deposit (CDs) earn 1-1.5% interest, while my portfolio on LendingClub is earning 6-7% interest. However, this isn't quite a bananas-to-bananas comparison, because part of your principal is repaid each month on LendingClub, and to maintain the interest rate advantage you have to reinvest it. Nonetheless, LendingClub has proven to be advantageous enough over traditional forms of banking and credit that in the past 7 years, since its inception, it has facilitated over $6B in loans.

I have been lending money via LendingClub for the past 5 years, and I have spent more time than any normal person would analyzing the investment potential of the service. In 2010, I blogged about applying a machine learning technique (called support vector machines) to help decide which loans to invest in. The results of this analysis supported the idea that LendingClub could persist as a viable service, because it showed that they were doing a substantially better job of analyzing the risks of loan default and appropriately setting the interest rate when compared to another P2P finance sevice called Prosper. My own experience lending money on both services was consistent with this result: my lending via Prosper yielded a return of 0.9% (as reported by Prosper) while my lending via LendingClub has yielded a return of 7% (as reported by LendingClub). I have since stopped investing using Prosper, though recently they have modified their approach to be more like LendingClub's.

Also in 2010, I sought to better estimate the returns that one could reasonably expect via LendingClub by analyzing the first batch of completed loans. The results from that analysis showed that LendingClub was exaggerating the expected returns: they advertised an average return of 9.65% while the first completed batch of loans actually earned lenders only 4.7%. I found this result startling, especially because it sharply contrasted with LendingClub's own claims for what the return-on-investment (ROI) should be. This difference made me skeptical about believing LendingClub's claims for lender returns, and this skepticism has stayed with me even as I have continued to lend with them.

Since then, LendingClub has stopped reporting an expected ROI for lenders. Their own analysis shows that their earlier batches of loans had a much higher default rate (~15% for loans originating in 2008) as compared with more recent loans (~6% for 2010). Remember, it takes 3 years for the true default rate on a batch of loans to be known, because they have 3-year terms. More recent data from 2012 suggest that the default rate is now above the 2010 level, though still below the 2008 level (see p.56 of the amended S-1). In general, I think one should expect a default rate within this range of 6-15% going forward.

Anyhow, enough history. The matter at hand is the IPO.

What the LendingClub IPO reveals about its business

As preparation for its IPO, LendingClub was required by law to release an amended S-1 (dated Dec 1, 2014). In this S-1 LendingClub set a price range for their offering ($10-$12/share), which would value the company at about $4B. I project revenue in 2014 of $219M and profit of $23M, which is a price-to-earnings ratio (PE) of 172. Rather than focusing on whether this valuation is justified, I'm going to take this time to share an insight into LendingClub's business that I did not realize until I read the S-1 a couple days ago.

In the S-1, LendingClub claims that its mission is to "transform the banking system" in part by "cutting out the middleman". My thesis in this post is that this is not true, that in fact, while LendingClub's history certainly involves cutting out the middleman between lender and borrower, its future looks more like providing a new channel of borrowers to the existing banking system. I would characterize this more as an "evolution" of the conventional banking system rather than a "transformation". One piece of data in particular supports this view, which I will now explain.

As described in the S-1, LendingClub makes loans available to lenders through 3 channels. The first channel is the LendingClub website (www.lendingclub.com), where a lender can go online to view individual loan applications and decide how much to lend to each borrower. Loans available through the website are called "Notes", and this channel clearly functions as a peer-to-peer service. The second channel is LC Advisors (LCA), where lenders can invest in LendingClub loans via ownership of Funds that hold loans. This channel is identified by "Certificates and Funds" in the S-1, and, asides from limiting the lenders that can participate, this channel functions at least partially as a peer-to-peer sevice, with individuals funding at least some of the loans. The final channel, which I was not aware of until I read the S-1, is a mechanism by which institutional investors, such as banks, buy whole loans. This channel is identified as "Whole Loan Purchases" in the S-1, and most definitely looks nothing like a peer-to-peer service. And this is the part of LendingClub's business that accounts for most of its loan growth in the past year (see Figure 1 below).

I was surprised to see LendingClub selling whole loans. The original spirit of the service was to allow individual lenders to diversify their investments by purchasing small parts (as low as $25) of larger loans (as high as $35,000). This approach seemed to appeal to the common man, because anyone could participate, the process was clear and public, and it wasn't just about the rich getting richer. This form of crowd-funding enabled the common man as the borrower to win (with a lower rate than their credit card), and the common man as the lender to win (with a higher return than they could get at the bank). In an age in which the conventional banking system not only profited from but was also disgraced for their involvement in the financial crisis of 2007-2008, this was a chance for the average American to participate once again in finance, on simple, understandable terms. But what seems to be happening instead is that LendingClub is just integrating itself into the existing banking scheme.

And finally, now, to the figures that say it all:

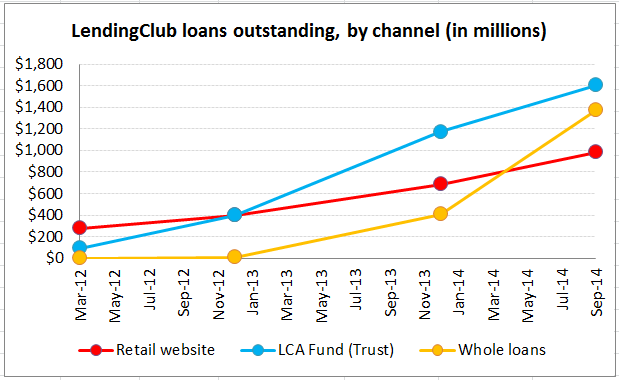

Figure 1: LendingClub loans outstanding, by channel (millions)

In Figure 1, I am plotting the outstanding principal balance of loans issued by LendingClub since March 2012, as reported in the table on page 58 of the S-1. Note that the numbers are outstanding principal as of the corresponding date, not the principal of new loans issued in that quarter. While LendingClub is experiencing substantial overall growth of 99% year-over-year (if I extrapolate linearly for principal outstanding at the end of the year for 2014 relative to 2013), the bulk of that growth has occurred not via the website (17%) or their LCA Funds (25%) but via whole loan sales to institutional investors (57%). If this trend continues in the next few years, whole loans could account for the majority of loans made by LendingClub. A P2P finance service, says who?

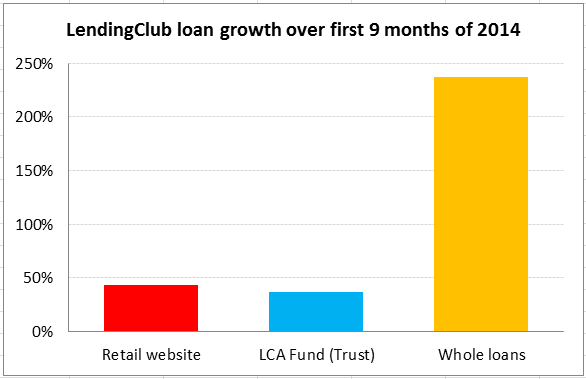

Figure 2: LendingClub principal outstanding growth over the first 9 months of 2014

Figure 2 above shows the growth in principal outstanding in the first 9 months of 2014. Whole loan principal has increased by 238%, website loan principal has increased by 43%, and LCA loan principal has increased by 37%. When I linearly project these statistics to annualized terms, they become 317%, 57% and 49%, respectively.

Conclusion

So what new things have I learned about LendingClub's business, having done this analysis?

- The majority of LendingClub's loan principal growth was due to sales via the whole-loan channel, NOT through growth in loans funded through the P2P channels (the website and LCA funds).

- If these trends persist, LendingClub in several years will no longer be a P2P finance service, but instead simply a new channel for banks to find borrowers. This assumes that the whole-loan category is primarily being funded by banks, which was not clear in the S-1.

- LendingClub appears to be executing a strategy whereby they maintain high growth rates by expanding into a new loan business each year. They did this in 2012-2013 with the LCA funds, and again in 2013-2014 with whole loans. I expect that they will again try to expand into a new credit market in 2014-2015, such as education, small business or medical loans, as demonstrated by their acquisition of Springstone.

- As a possible investor after LendingClub's IPO, your faith in the company should depend on your belief that they will be successful in expanding into new markets, NOT just growing existing ones. This is different than other companies, such as Google and Facebook, who simply had to grow an existing revenue source (online advertising on their own websites) rather than having to expand their technology into new markets (e.g. if Google had to grow by entering the television ad market). My personal experience using LendingClub to lend for small businesses, medical procedures and education ended with a much higher default rate than lending to people who were refinancing their credit cards or other debt. Hence I am skeptical about the success that LendingClub will have expanding into these markets.

Hopefully you found this analysis interesting, and perhaps useful. I sure feel like I have a better sense of the LendingClub business now, which guides my sense for how to value the company as the IPO approaches.

---

Relevant link:

LendingClub's S-1 at sec.gov

No comments - Write 1st Comment

« Assumption

-

Rain »

|